Bouncing This Week

But if youre the piano player, time to sneak out

The sentiment for 2025 is wildly optimistic. It hasn’t been this much cheer since the end of 2019.

And yet, the backdrop, the everything bubble, whose top is lining up with the clash of the century, literally, of the globalist entities vs. the individual. Yes, the battle has been brewing and taking form for some time now, but what’s different, is the individuals now, with momentum behind them on both of the major continents of the Western World, are also ready to fight to the death.

Usually I avoid politics. I care about as much about politics as a do, say, professional basketball, which is to say I don’t.

There it is — the strongest words in any language. Je m’en foustisme. I don’t care.

But this is different now, because of the timing, on how one facet - the economic one, coincides with and catalyzes the other - the cultural political one.

Quel bordel! as mom used to say.

And just where does all this optimism emanate from? The prospect that somehow, corporate earnings will continue increasing unabated? Even though, if they doubled, it would put PEs simply at historically normal levels?

This time is different, right?

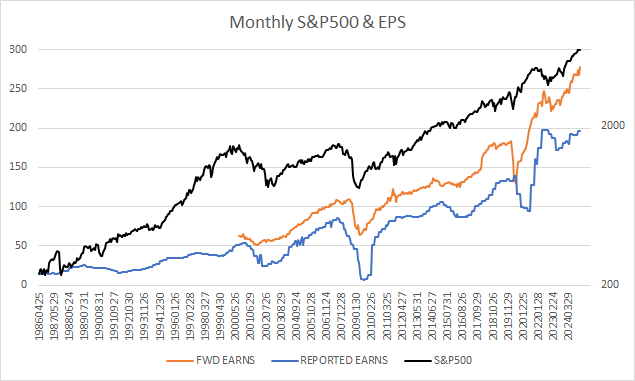

Look at this chart, showing forward earnings, the perpetually, overly-optimistic exosmose from corporate PR spinners to analysts, versus the actual, reported GAAP-certified earnings:

Notice that, since May of last year, the fictional forward is charging on to new highs, the actual, struggling to surpass the highs of early ‘22.

That is one ugly divergence there. The fact is, for all the whoop-a-la, the earnings are really coming in as planned the past 9 months.

And employment, the main driver of equities, is really, really sick here.

So valuations are ridiculous, employment is ill, sentiment is extremely overly-bullish (referring to the last communique’s chart of percentage of household net worth in equities, not to mention the year-end financial news), and, the coup de grace, in terms of major bear market timing, the normalization of the yield curve:

Anyone who speaks of lower rates being healthy for stocks here, is not a student of history. Look at what has happened in the chart above, every time we got an inversion, then things started normalizing — all hell broke loose in equities (even the “pandemic” selloff, telegraphed in August of 2019 by the 90-30 curve)

I know, I know…this time is different.

In so far as the credit markets are concerned, we will know it is really starting to melt down when the credit quality spreads start receding, and they will, and likely in the next couple of months.

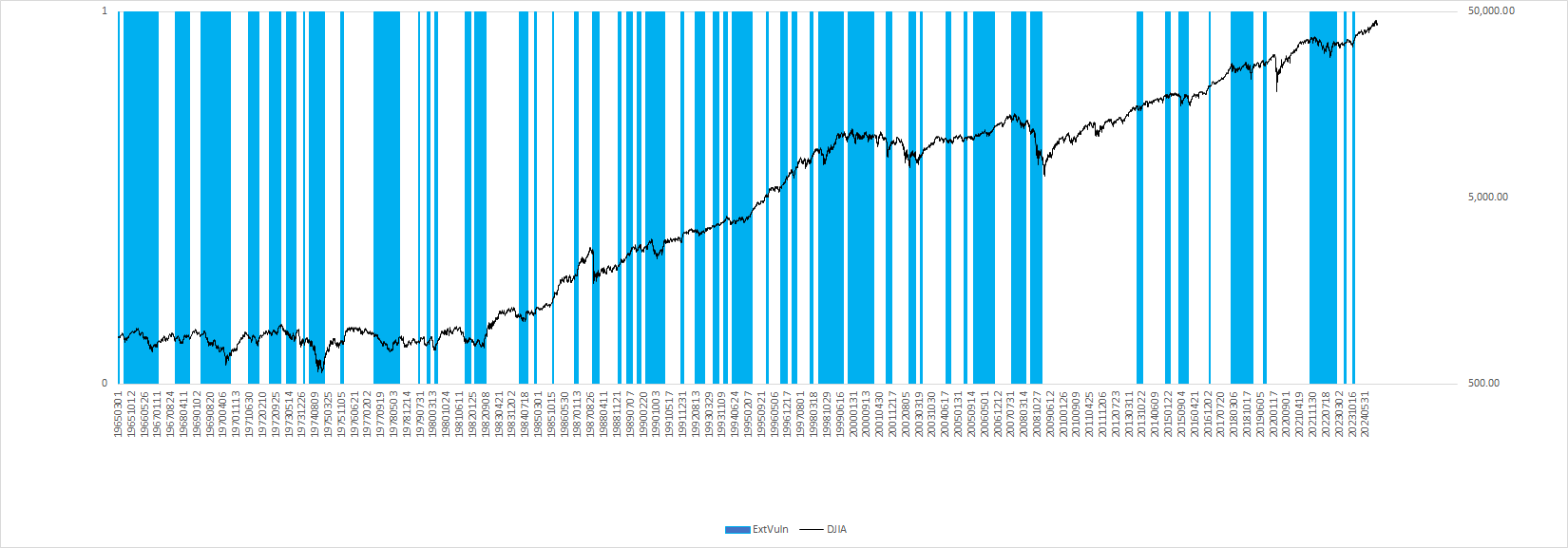

Next, let’s examine what I call “Periods of Extreme Vulnerability,” in the blue bands, below:

Notice that every major selloff / bear market in the past half-century, transpired in a period of extreme vulnerability (this is discussed in my Charles H. Dow award winning paper, along with the 4% rule, the “Bloodbath Indicator”). We are about 2 weeks away from entering a fresh, new period of extreme vulnerability unless we have a day in the interim that sees single-digit daily new lows on NYSE stocks.

Lastly, since are covering the bases of the major drivers in equities, the Fed, though backing off on rate hikes at the moment, QT continues quietly in the shadows (save for having to rescue their cronies at SVB bank, inflation be damned. It was as if Hank Paulsen himself was reincarnated as Janet Yellen [Is he dead? J m’en foutisme.] ):

A nasty brew is boiling in all the pillars the drive the equities markets, right as we head into a period of extreme vulnerability, right as the yield curve, which was bent over for over a year, for an historically long time, normalizes.

Do you really want to be on the side wagering that “This time is different?”

Now, shorter-term, we’re certainly due for a bounce, and likely one of the “Rip your face off,” variety, starting this week. Once again, we got down to only 6 of the past 20 days in the DJIA being up:

And from such points, healthy bounces have happened. When they happen in a bear market, they tend to be violent to the upside.

Further on the short-term, using the powerful Vantage Point Software, we are cming off of a volume bar bottom week the week of 20 December, and have a cyclical bounce into the week of 24 January (+ or - 1 week), based on the currently dominant 13-15 week cycle.

(I tout Vantage Point Software because I use it, and think it’s worthy of my readers looking into. Of late, another fellow I am aware of who has a hell of a futures trading track record going on , Kelley Michael Wallace, who has his money management software, which I am familiar with and like very much, offered at https://kwallacemoneymanagement.com/ . It’s worth a look.)

I doubt, however, given the beating most stocks are already sustaining now, that such a short-term bounce will be enough to likely avert the coming period of extreme vulnerability (which, oddly, lands on the calendar right around the time of The Inauguration).

Yes, stocks have been getting hammered, for the most part, especially in certain European markets as well as the US (France, for example, was down for 2024). If you take away the Magnificent 7, the US was down too.

The selectivity being highly symptomatic of a final stage bull market (which certainly coincides with the normalization of the US Treasury yield curve). In fact, there is "selectivity" occurring now in all asset classes of the final stage "everything bubble," be it real estate (commercial has been hammered, residential performance by locale), art, collectibles (look at the buying panic in luxury watches of a few years ago, now being led by only a single brand), even crypto. Everyone points to TC and the limitless price prognostications there, but where is ETH relative to its all-time-high? How about the litany of other coins? How about NFTs for cryinoutloud?

That said, the data is quite clear, as has been posted here in recent months, that we are in for a 50-80% decline this decade (which will be the economic defining event of the decade) in US stocks. That's not to say we have entered into it (I don't think so, yet), but given the magnitude of this (I am not trying to be hyperbolic, it’s just what the numbers show) certainly it’s important to err on the side of caution in this era. It will be a transformative event, and an extinction event for many institutions.

The cultural shift we are witnessing, across the entire Western World and Latin America, is ignored or downplayed by us at our peril. The undercurrent of all of it being the clash of Globalism versus the Individual, and it cuts across all aspects the former sought to create division in. When Bernie Sanders is calling for the same individualistic buttressing as the J6ers as the young women casting their votes in the US elections based on “Reproductive Rights,” an alignment has taken place. In an an expected - or unexpected, turn of events, the President-elect, despite all odds, slings, arrows, bullets, gag-orders and floozies, wins by a powerful, popular majority, them squanders a critical mass of it before he is even inaugurated. Simultaneously, in the most perverse optics conceivable, hands out sinecures to wealthy donors while, again, whether you find the felons or martyrs, the J6ers who were clearly the most ardent of his base, rot in prison.

The globalist blob, smelling blood, with enough of his support now squandered, will waste no time taking this Presidency apart. Thune is already speaking how Trump’s cabinet nominees man not get through.

As I predicted last Summer that Trump would get elected resoundingly, now I doubt his Presidency will last a year. We may be right back in 69 A.D. and go through several of them in short succession, especially as financial markets take it on the chin, with one element causing further damage to the other in a feedback loop of trouble.

The President-elect flirts with the global cabal here, and his base, clearly understanding what the President-elect doesn’t seem to, that the over-arching battle is the globalist blob versus the individual, and they will have none of this, and none of him very shortly. Only a hat-in-hand speech to his base can turn this around now.

The momentum, everywhere, is on the side of the individuals and those politicians who understand this and support it. The blob can, and always could, handle fear-induced individuals, but that is no longer the case. The more the markets melt down, the more damaged and lame the blob becomes.

And in that vein, with so many having lost their life savings and retirement, underwater on houses if they were lucky enough to afford them, the momentum on the individuals and the dissipation of fear increases. The doctrine of the blob is finished - DEI is dead in America, having been in the death throes for a year, with the singlemost incompetent DEI hire of all time, the first female Vice President of the United States. I suspect

Yes, she really was. Hard to believe, isn’t it. I wish i could say “I don’t care,” but it’s too grotesquely embarrassing that such an affront to our sensibilities was permitted.

The coming litigation on DEI will dwarf that of the big tobacco. Oh, I know, lawyers for these globalist, blob entities will shot back to me to justify

on what legal basis I can say that. I am not an attorney. Nor am I a biochemist, but you knew those pending tobacco lawsuits, or even their enfeebled cousins, the asbestos ones, were going to cripple the defendant globalblob companies. Likewise, the attorneys of these entities - who know it’s inbound, somehow want to pretend tht whistling past the graveyard might prolong the inevitable.

But you know it’s coming. This time is not different. The racial and gender discrimination of these entities has a price tag attached that’s going to come due. The individuals, with their momentum, which only increases under financial stress, will demand it. Ten years from now, you’ll hear the names of these entities, investment banks and electronic exchanges, and wonder how they could have fallen so far.

And that, folks, is how we will know it’s time to begin looking for a bottom.

Conclusions and Strategy